10F, Building B, Erqi Center, Erqi District,

Zhengzhou City,

Henan Province, China

Wit:+86 15138685087

(WhatsApp/Wechat)

10F, Building B, Erqi Center, Erqi District,

Zhengzhou City,

Henan Province, China

Wit:+86 15138685087

(WhatsApp/Wechat)

(Reporter Yang Yue) May 9, London time, the World Steel Association released the April 2024 version of the short-term steel demand forecast report, expects global steel demand in 2024 to rebound by 1.7% to 1.793 billion tons; global steel demand in 2025 will grow by 1.2% to 1.815 billion tons. 2024-2025, the global steel demand will continue to grow.

World Steel Association

As far as China is concerned, WSA expects Chinese steel demand in 2024 to remain roughly at the 2023 level. Although the continued decline in real estate investment has led to a corresponding contraction in steel demand, demand growth from infrastructure investment and the manufacturing sector will offset the decline in the real estate sector; in 2025, Chinese steel demand is expected to decline by 1%, well below the peak demand in 2020.

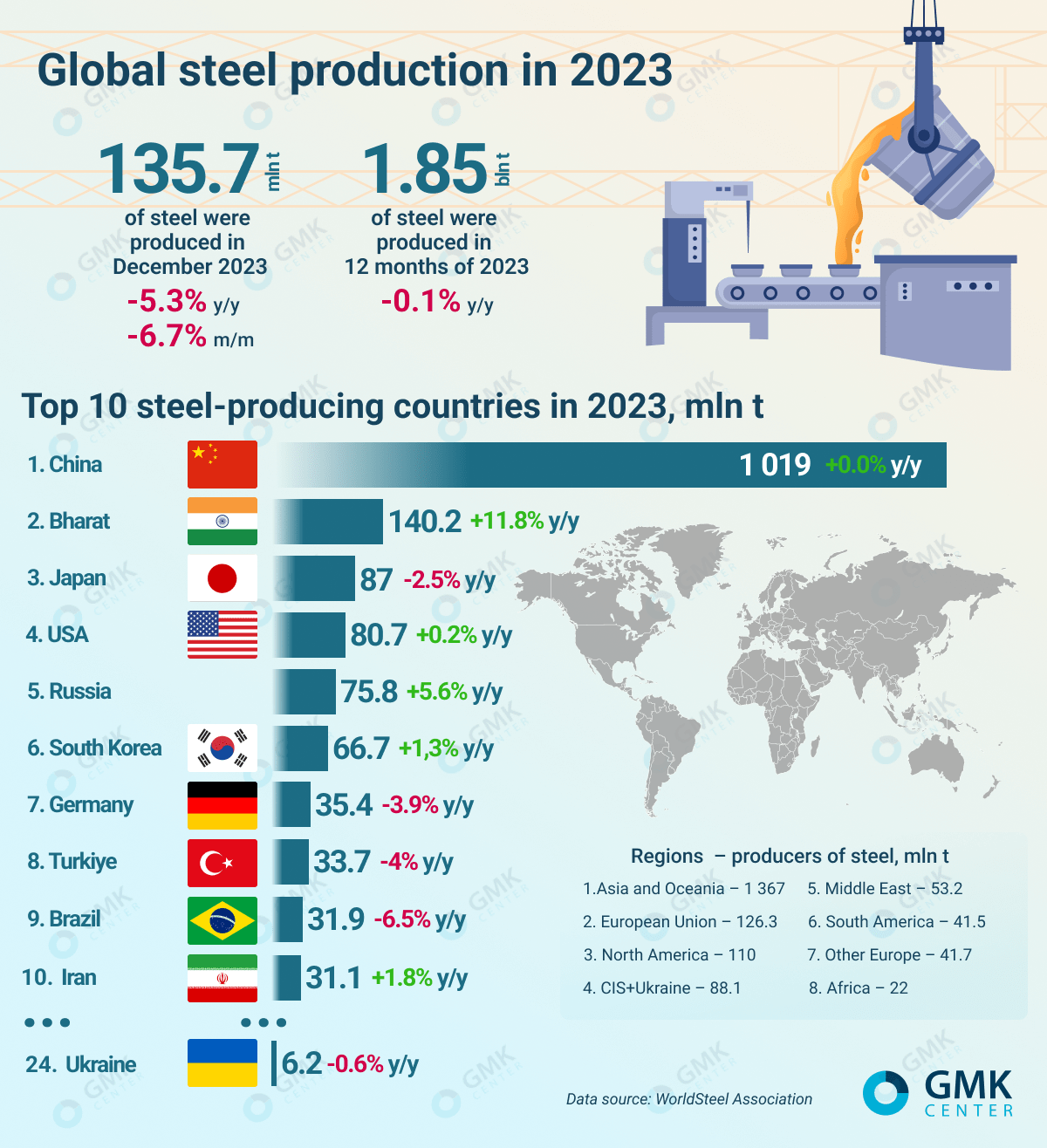

gloable steel production in 2023

Information Source: 《 GMK CENTER 》

In 2024-2025, global steel demand in countries other than China is expected to grow by 3.5% per year.

Specifically, in 2024-2025, affected by local infrastructure investment, India’s steel demand will continue to grow by 8%, and steel demand in 2025 is expected to be nearly 70 million tons more than in 2020.

Edwin Basson

Yu Yongzheng delivered a speech

Following the slowdown in growth in 2022-2023, the Middle East, North Africa ASEAN, and other emerging economies’ steel demand is expected to accelerate in 2024-2025, of which ASEAN is affected by political instability and other factors.

The future growth rate of steel demand is expected to slow down further; the steel demand in developed economies will grow by 1.3% and 2.7% in 2024 and 2025, respectively, of which steel demand in the EU is expected to see a substantial recovery in 2025, the U.S., Japan and South Korea will also maintain steel demand resilience.

steel coil

car structure

It is worth noting that the EU and the UK remain the most challenging regions for global steel demand growth. The steel industry in the EU and the UK, facing many challenges such as geopolitical change and uncertainty, high inflation, monetary tightening, and the removal of some fiscal support, as well as high energy and commodity prices, will see steel demand fall sharply in 2023 to its lowest level since 2000.

Steel workshop

production line

The forecast for 2024 will be revised downwards sharply, with signs of recovery only expected in 2025, with a growth rate of 5.3 percent.

U.S. steel fundamentals are still strong and are expected to return to a rapid growth trajectory in 2024.

From a downstream industry perspective, on the one hand, high interest rates and high construction costs have led to a downturn in the residential construction sector, dragging down demand growth in most major steel-consuming regions.

bundles of steel wire

steel processing plant

With poorly motivated activity in the residential sector in the US, China, Japan, and the EU in 2023, compounded by the impact of tightening currencies, and with a substantial recovery in demand for steel in the residential construction sector expected to start only from 2025.

Head of the Steel Association

world steel conference

On the other hand, high costs, high uncertainty, tighter financing conditions, and weak global demand have led to weak global manufacturing activity, and the automotive industry in most countries is expected to show a weak growth trend at best in 2024.

In addition, the World Steel Association believes that the sizeable green transformation of the world economy is one of the main reasons for strong investment in the public infrastructure sector.

For example, a recent study conducted by the World Steel Association’s Market Research Committee suggests that new wind power installations will drive a three-fold increase in global steel demand to around 30 million tons by 2030, compared to the early 1920s.

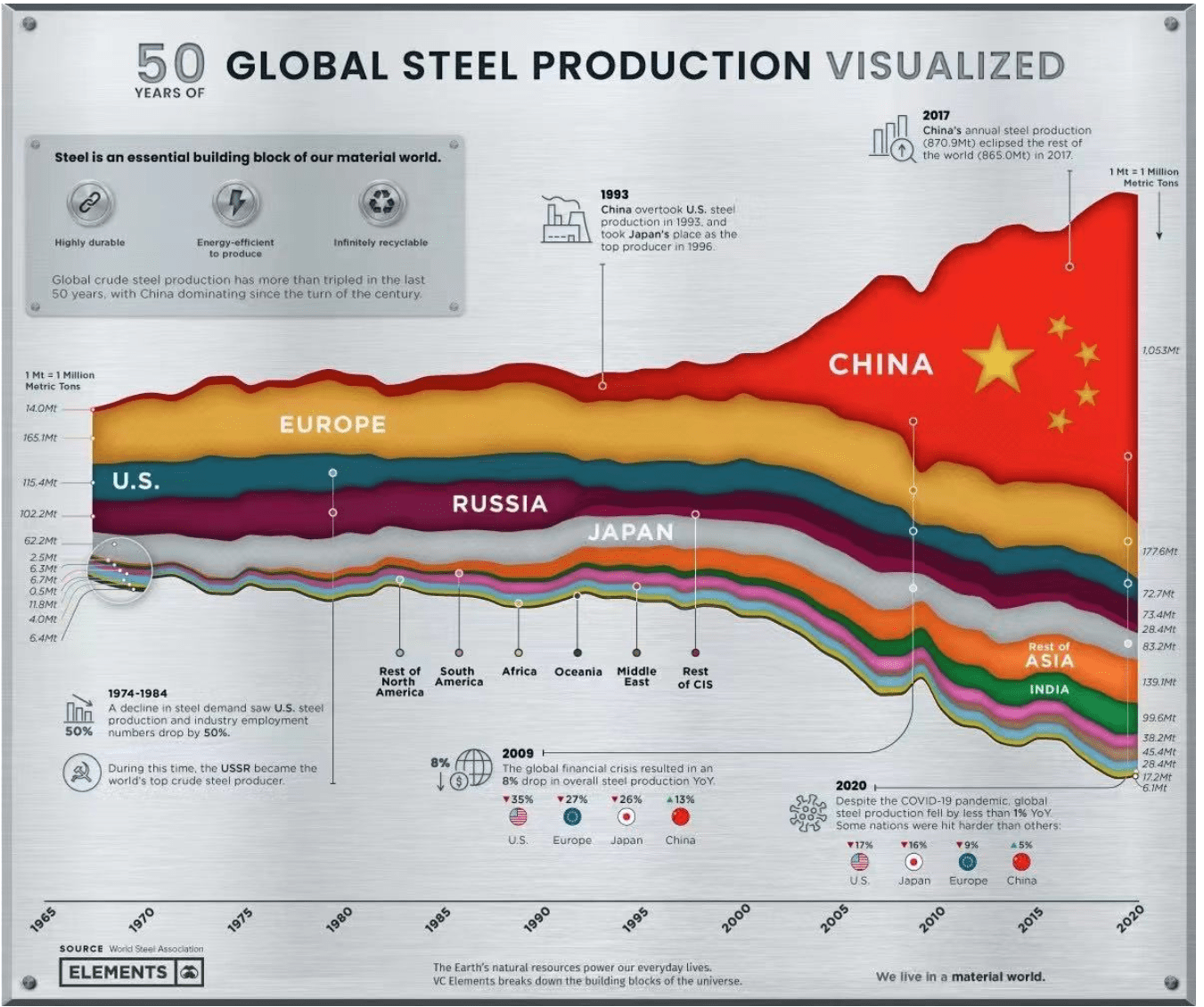

History of China’s Steel Production

Although the share of steel demand from the wind energy sector in total global demand is relatively small, it is likely to support overall steel demand in regions such as Europe.

It is important to note that those public infrastructure investments aimed at strengthening infrastructure development, climate change risk resilience and post-disaster reconstruction are important factors that will support steel demand growth in 2023 in major steel-using countries such as Japan, South Korea and Turkey.

Galvanized steel coil

steel worker

The World Steel Association emphasizes that while public infrastructure investment and manufacturing investment will remain strong, high construction costs and labor shortages may constrain future public infrastructure investment and manufacturing investment growth in the short term.